A Guide to Reading Your Credit Report

Your credit report is the basis for your credit scores, and what many creditors want to review before approving your application or determining your rates. Being able to read your credit report (and understanding what you’re reading) is important if you want to improve your creditworthiness.

Credit reports are broken up into different sections. The exact names and order can vary, but they’re generally similar to:

- Summary

- Personal information

- Credit accounts

- Collections

- Statements

- Public records

- Inquiries

Here’s what you may find in each one. We’ve even included images from an anonymized credit report (with the person’s permission) to show what’s in the report and explain how to read it.

Your report will look different depending on if it’s your Equifax, Experian, or TransUnion credit report. Even then, two reports from the same credit bureau may look different depending on which service you used to get your report.

The images in this guide come from Equifax and TransUnion credit reports from AnnualCreditReport.com, and an Experian credit report from Experian.com.

Summary

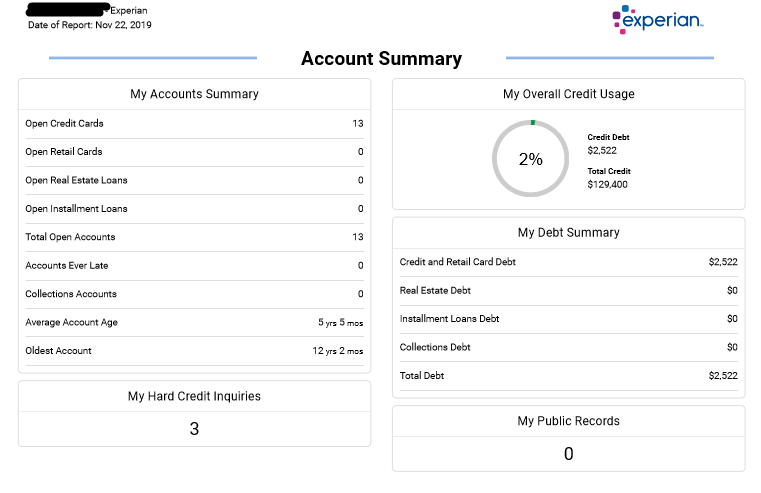

Your credit report will often start with a summary section. The information in this section often mirrors several of the factors that determine your credit scores, such as the average age of accounts, the types of accounts in your report, and your overall credit utilization rate.

The Experian credit report shows your overall credit usage (also known as utilization rate) in the account summary, which is an important factor in your credit score.

The Experian credit report shows your overall credit usage (also known as utilization rate) in the account summary, which is an important factor in your credit score.

Some summaries may be more detailed, listing the balances by account type, your oldest account, most recent account. In some cases, you may receive a report without a summary section. But don’t worry, while a summary can give you a nice overview, you’ll want to focus on the meat of the report.

Personal information

The personal information section is sometimes part of the summary section, or appears later in your credit report. This is where you’ll find your name, aliases, date of birth, Social Security number, phone numbers, addresses, and employers. The data comes from the applications you’ve previously submitted, and your current credit accounts.

![]() A personal information section from a TransUnion credit report lists several addresses.

A personal information section from a TransUnion credit report lists several addresses.

While the information in this section won’t impact your credit scores, you still want to make sure everything is accurate.

If there’s a name or address that you don’t recognize, that could be an indication that someone has stolen your identity and is using your information to open a credit card or take out a loan.

Credit accounts

The accounts section can be the most important—and lengthiest—part of your credit report. This is where you’re going to find all your credit accounts, details about the accounts, and each account's payment history.

Carefully read and review each account for errors. A negative mark, such as a late payment when you paid the bill on time, could hurt your credit score for years.

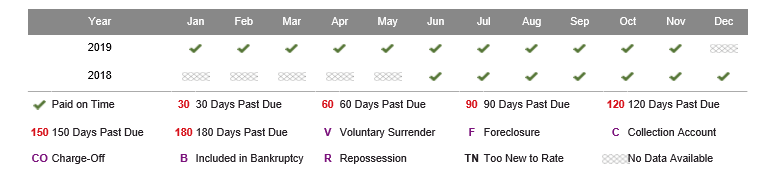

![]() TransUnion’s legend explains what the symbols and letters in the account’s payment history mean.

TransUnion’s legend explains what the symbols and letters in the account’s payment history mean.

Equifax’s is similar, but uses different markings and letters.

Equifax’s is similar, but uses different markings and letters.

If you look at the legends closely, you’ll see there’s no mark to indicate you were one day late, or even 10 days late, with a payment.

Tip: Creditors shouldn’t report your account as late unless it’s been 30 or more days past the bill’s due date.

You may have to pay a late fee or interest charges if you’re one day late, but bringing your account current before the 30-day mark allows you to avoid negatively impacting your credit scores.

Back to reading your credit report—the accounts section may be split between open and closed accounts. It may also separate different types of accounts, such as credit cards, mortgages, and installment loans. If you have other types of accounts reported to the bureaus, such as rent or utilities, they may be in a separate section as well.

An open credit account can stay on your report indefinitely. Here’s what an open account looks like on a TransUnion credit report.

![]() An open credit card account on a TransUnion credit report. The scheduled payment was for the minimum amount due, but the balance was paid in full each month.

An open credit card account on a TransUnion credit report. The scheduled payment was for the minimum amount due, but the balance was paid in full each month.

Closed accounts can remain on your credit report for 10 years after they’re closed if they were in good standing (i.e., fully paid) at the time. Here’s a closed credit card account on a TransUnion credit report.

![]() The TransUnion credit report has a credit card that was closed in 2013 (the date closed is in the top left). The months that have an X rather than OK are the result of the card going unused. There was no payment due, so the payment was neither on time or late.

The TransUnion credit report has a credit card that was closed in 2013 (the date closed is in the top left). The months that have an X rather than OK are the result of the card going unused. There was no payment due, so the payment was neither on time or late.

If you were behind on payments when an account is closed, it will fall off your credit report seven years after the original late payment that led to the closure.

For example, if you were late on a credit card payment in May 2014, and you never brought the account current, the credit card company may eventually close your account and send it to collections. The entire account and related collections account will fall off your credit report in May 2021—seven years after the original delinquency was reported.

Collections

If your creditors have sent an account to a collections agency, the collection account will appear in a separate section of your credit report.

Collections accounts can have a negative impact on your credit scores, and they’ll remain on your credit report even if you pay off the past-due balance. They’ll fall off with the related account seven years after the original delinquency date, which should be listed next to the collection account.

Statements

You can add a short statement to your credit report. Often, this may be an explanation for something that looks odd in your report or for why you were late with a payment. However, while negative marks will eventually fall off your credit report, the statement might stay put.

If you choose to add a statement, also set a calendar reminder to remove statements that reference negative marks. Otherwise, you may be tipping off creditors that there was a late payment when none appear in your report.

Public records

Most information in your credit report comes from companies sending data to the credit bureaus. However, credit bureaus also collect or purchase public records information from the court systems.

Previously, these included judgments and liens. However, the credit bureaus decided to remove those public records from credit reports in 2017 and 2018.

Now, this section is where you’ll find bankruptcy records. Depending on the type of bankruptcy, it will fall off your credit report after seven years (for a Chapter 13) or ten years (for a Chapter 7) from the filing date.

A bankruptcy in your credit report can severely hurt your credit scores. Although, as with other negative marks, the impact decreases over time.

Scores aside, the bankruptcy can also impact your overall creditworthiness as creditors may be reluctant to lend you money if you’ve declared bankruptcy in the past.

Inquiries

A credit inquiry gets added to your credit report whenever someone looks at (sometimes called “pulls” or “checks”) your report. There are two types of inquiries—soft inquiries and hard inquiries.

|

Soft Inquiry |

Hard Inquiry |

|

|

Impacts your credit scores? |

No |

Sometimes lowers your scores by a few points |

|

Appears on your credit report when someone else gets a copy? |

Usually no |

Yes |

|

Results from you giving permission for a credit check? |

Sometimes |

Always |

A soft inquiry can happen when:

- You check your own credit report.

- You apply for a prequalification or preapproval with a soft credit check.

- An employer reviews your credit as part of your interview process.

- One of your current creditors checks your credit for account maintenance purposes, such as determining if it should raise or lower your credit limit.

- A creditor sends you a firm offer of credit, such as a mailer asking you to apply for a new credit card or loan.

Soft inquiries never impact your credit score. In fact, these inquiries generally only appear on the copies of your credit report that you receive.

![]() TransUnion separates soft inquiries into different types depending on the reason for the inquiry.

TransUnion separates soft inquiries into different types depending on the reason for the inquiry.

On the other hand, hard inquiries can hurt your credit scores. Often, there’s only a slight drop (such as five or fewer points) from a single hard inquiry, and the impact diminishes over time.

Hard inquiries happen when:

- You apply for a credit card, loan, or another type of credit account.

- Applying for an apartment can sometimes lead to a soft or hard inquiry.

If you apply for a loan through a middleman, such as a mortgage broker or car dealership’s finance office, you may see many hard inquiries from the company shopping around to find you the best rate. The companies that make credit scores understand that shopping for a loan is a good idea—not risky behavior—and may combine inquiries that happen during a short period when calculating your scores.

It’s also common for there to be different inquiries on your credit reports from the three credit bureaus, as many creditors will only check one of your reports while reviewing your application.

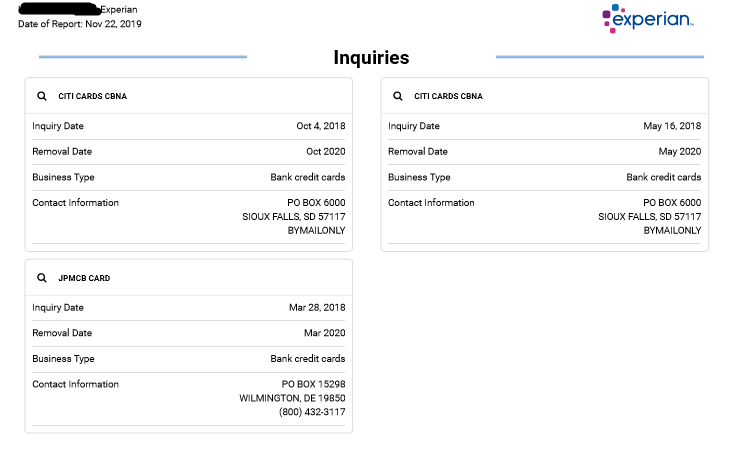

The inquiries section from an Experian credit report doesn’t contain any of the soft inquiries listed in the TransUnion report above. However, it has three hard inquiries that weren’t in the TransUnion report.

The inquiries section from an Experian credit report doesn’t contain any of the soft inquiries listed in the TransUnion report above. However, it has three hard inquiries that weren’t in the TransUnion report.

Both soft and hard inquiries will remain on your credit report for two years. The hard inquiries may impact your scores during the entire two years, although FICO credit scores only consider them during the first 12 months. Often, your scores can recover from a hard inquiry within a few months.

What If Something Is Incorrect?

One reason to review your credit report is to look for errors. If you spot a mistake, you can file a dispute with the credit bureau, which then has to investigate your claim.

The bureau will then reach out to the original creditor and validate the information, correct the error or delete the information. Your credit scores can improve when a disputed negative mark gets corrected or deleted.

Some mistakes are glaring—such as an account you didn’t open or a late payment when you’re positive you paid on time. However, there can also be subtle mistakes, such as an incorrect past-due amount or the wrong date on a payment.

Credit Saint, a credit restoration service, specializes in carefully reviewing credit reports for mistakes. We can help you understand what should be in your report, dispute errors that may be hurting your credit scores, and take steps to add positive information to your credit.

Our customers generally see a change in their scores within 45 days, and we offer a money-back guarantee if you don't see any deletions in the first 90 days.